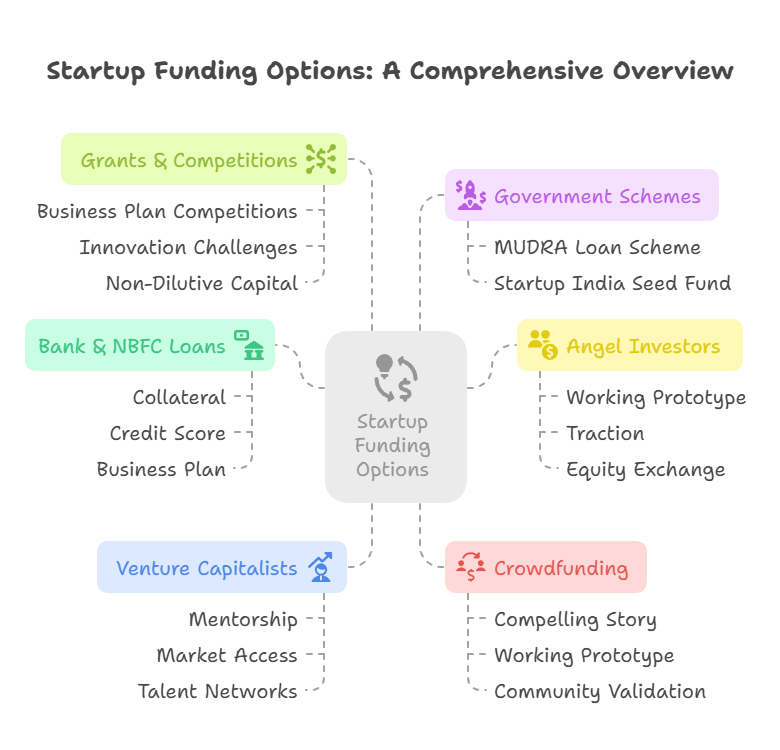

Banks typically require a business plan, KYC documents, cash flow projections, collateral details, and in some cases, a valuation report. NBFCs may offer more flexible terms, but credible financial documentation from a trusted advisor like Marcken Consulting will strengthen your application.