Table of Contents

Toggle1.Introduction: Why Valuation Fees Matter

Valuation is no longer a niche exercise in India—it has become a core requirement for businesses across sectors. Whether it is a startup raising its first round of funding, a listed company navigating a merger, or an enterprise issuing ESOPs to its employees, independent valuation plays a critical role. In fact, under the Companies Act, SEBI regulations, RBI guidelines, and various tax laws, valuations are often not optional but mandatory.

In this environment, the question of “what does a company valuer charge for valuation?” is more than a matter of curiosity. For founders, CFOs, and boards, understanding fee structures ensures better financial planning, regulatory compliance, and transparent engagement with valuers. For investors and regulators, transparent fee disclosures help reinforce confidence in the fairness and independence of the valuation process.

As India’s valuation ecosystem matures, knowing the cost benchmarks for 2025 helps businesses avoid surprises, negotiate effectively, and budget appropriately for transactions or compliance exercises.

2.Key Factors Influencing Valuer Charges

The cost of engaging a company valuer is not uniform—it varies depending on several interlinked factors. While the regulatory framework provides broad guidelines, market practice and institutional policies also play a decisive role. The following considerations are central to how valuation fees are determined:

1. Nature of the Asset

The type of asset being valued is one of the primary determinants of fees. A straightforward property valuation will typically be less expensive than valuing an entire business with multiple subsidiaries or intangible assets. For instance, goodwill, intellectual property, and complex financial instruments demand specialised expertise, which directly reflects in higher professional charges.

2. Complexity of the Assignment

Valuations differ widely in scope and technical depth. A compliance-driven ESOP valuation is less intensive than a cross-border M&A deal that requires scenario modelling, sensitivity analysis, and benchmarking across jurisdictions. The more intricate the assumptions, modelling, and documentation, the higher the professional input—and therefore the cost.

3. Regulatory Requirements

Fees are also guided by statutory frameworks. Registered valuers are often required to follow scales prescribed under the Wealth Tax Rules or adopted by institutions under the Companies Act. These create a sliding scale based on the value of assets, ensuring proportionality in charges. Additionally, regulatory audits and peer review standards mean that valuers must devote considerable time to compliance and documentation, which influences their pricing.

4. Institutional or Industry Fee Caps

Banks, financial institutions, and sometimes regulators set fee ceilings or slab-based structures to maintain uniformity and prevent excessive charges. For example, public sector banks may impose caps of ₹1.5 lakh on valuation fees, regardless of the asset’s size. Industry practice also influences expectations—valuation firms catering to startups may adopt flat-fee models to suit limited budgets, while those advising large corporates follow percentage-based or tiered pricing.

3.Regulatory Fee Framework for Registered Valuers

In India, the charges levied by registered valuers are not arbitrary; they are guided by a structured framework. The benchmark often referred to is Rule 8C of the Wealth Tax Rules, which has, over time, been adopted in various contexts for company law and institutional valuation purposes. This ensures consistency and fairness in determining fees, while also offering businesses predictability.

The framework prescribes a sliding scale of fees, calculated as a percentage of the asset value:

- On the first ₹5,00,000 of asset value: 0.5% of value

- On the next ₹10,00,000: 0.2% of value

- On the next ₹40,00,000: 0.1% of value

- On the balance amount: 0.05% (i.e., 1/20th of 1%) of value

Additionally, a minimum fee of ₹500 is applicable, ensuring even smaller assignments attract a base level of compensation for the valuer.

This tiered approach ensures that valuation costs remain proportionate: smaller businesses are not overburdened, while larger assignments reflect the additional responsibility and professional effort involved.

4.Worked Example of Fee Calculation

To illustrate how this sliding scale operates in practice, let us consider a business with an assessed value of ₹70 lakhs. The valuer’s fee would be calculated step by step, applying the relevant percentage at each slab:

- First ₹5 lakhs at 0.5%: ₹2,500

- Next ₹10 lakhs at 0.2%: ₹2,000

- Next ₹40 lakhs at 0.1%: ₹4,000

- Balance ₹15 lakhs at 0.05%: ₹750

This worked example demonstrates how a structured framework leads to transparency and predictability. For businesses, especially SMEs and startups, such clarity allows them to budget for compliance-related costs without the risk of arbitrary pricing.

Institutional Caps and Bank Fee Structures (2025)

While registered valuers often follow prescribed scales, banks and financial institutions have introduced their own fee ceilings to standardise costs across borrowers and regions. For instance, in 2025, the Bank of India implemented a maximum cap of ₹1.5 lakhs on valuation services. This means that even if the asset value is very high, the valuer cannot charge more than the capped amount when the assignment is for the bank.

In addition to such upper limits, many public sector banks use slab-based fee structures depending on the property or business value. These may include:

- Smaller businesses: ₹5,000 – ₹10,000 per valuation

- Medium-scale assignments: ₹25,000 – ₹50,000

- Larger cases: Higher fees, but always subject to the institutional cap

Such measures are designed to prevent overcharging and maintain uniformity, especially in cases where valuations are necessary for lending or regulatory purposes. For borrowers, this offers cost certainty, while for companies, it means valuations tied to loans or institutional requirements may be more affordable than private-market valuations.

Private Valuation Firms: Market Practice

Beyond regulated or institutional mandates, private valuation firms operate under more flexible fee models that combine flat fees and value-linked percentages. Their pricing is often tailored to the type of client, complexity of work, and the purpose of valuation.

Typical market practices in India (2025) include:

- Early-stage startups: Flat fees ranging from ₹25,000 to ₹1 lakh for assignments such as ESOP valuations, investor reporting, or basic compliance-related reports.

- Mid-sized companies: ₹50,000 to ₹2.5 lakhs, depending on the depth of due diligence, financial modelling, and report customisation required.

- Large enterprises or listed companies: ₹2 lakhs to ₹10 lakhs or higher, particularly for complex assignments like Purchase Price Allocation (PPA), cross-border M&A, or valuations involving multiple subsidiaries and asset classes.

In addition, some firms offer discounts for repeat or group assignments and may bundle valuations into annual compliance packages. This flexibility allows companies to negotiate terms and choose a model that best aligns with their scale and financial capacity.

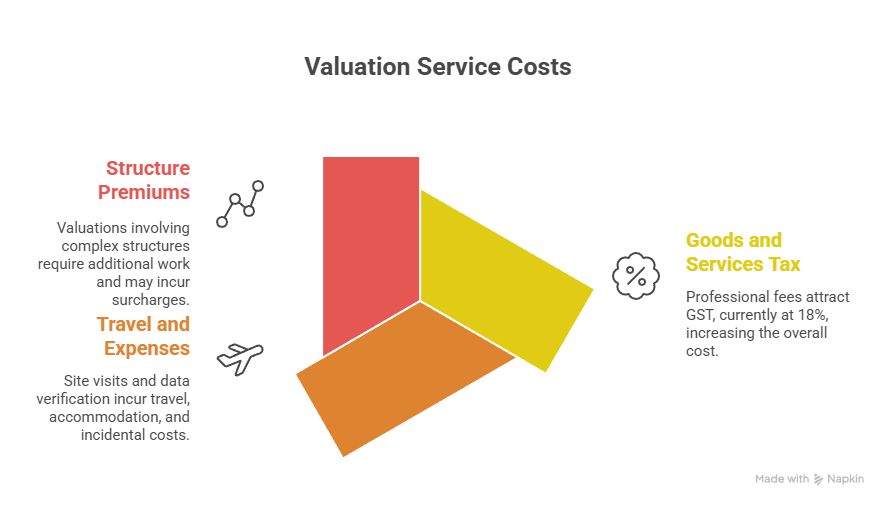

Additional Cost Components

When budgeting for valuation services, it is important to consider that the headline fee is not always the final cost. Several additional components may apply, depending on the nature of the engagement:

- Goods and Services Tax (GST): All professional fees attract GST at the prevailing rate, currently 18%, which can significantly increase the overall outlay.

- Travel and Due Diligence Expenses: If the assignment requires site visits, management interviews, or extensive data verification, the valuer may bill for travel, accommodation, or other incidental costs. These are usually charged on an actuals basis, over and above the professional fee.

- Multi-Entity or Group Structure Premiums: Valuations involving holding companies, subsidiaries, or multiple asset classes often require additional work. Firms may apply a surcharge or a higher base fee to account for the extra complexity in consolidating results and ensuring compliance.

By anticipating these cost elements upfront, companies can avoid unexpected additions to their valuation budgets.

Complex Assignments and Premium Pricing

Not all valuations are straightforward. Some transactions and compliance requirements call for specialised expertise and more intensive analysis, which naturally command premium pricing. Common examples include:

- Business Combinations (M&A, PPA): Mergers, acquisitions, and Purchase Price Allocation (PPA) exercises often involve valuing multiple asset classes, intangible assets, and goodwill, all of which demand rigorous modelling and documentation.

- ESOP Valuations and 409A-Style Compliance: Employee stock option schemes and fair value certifications for equity-linked compensation require independent valuations that withstand both regulatory and investor scrutiny. These typically involve detailed financial forecasts and peer benchmarking.

- Cross-Border and Multi-Jurisdiction Valuations: When companies operate in multiple countries, valuers must address international accounting standards, foreign exchange dynamics, and cross-border tax implications. This makes such assignments particularly resource-intensive and significantly more expensive.

- Premium assignments such as these highlight why valuation fees can range widely—from modest compliance-driven exercises to multi-lakh or even crore-level engagements for large corporates.

Negotiation and Flexibility in Fees

Valuation fees are not always rigid. Many firms, especially private valuers, offer room for customisation and negotiation, depending on the client’s profile and the scope of work:

- Scope-Based Discounts for Startups: Early-stage companies with straightforward capital structures may negotiate lower fees. Some valuers extend discounted packages specifically designed for seed and Series A startups.

- Fixed Fee vs Milestone-Linked Models: While most engagements are billed as a flat fee, milestone-linked billing is also common—particularly for long-duration projects like M&A or fundraising that may involve multiple deliverables.

- Equity-Linked Fee Arrangements: In rare cases, especially with venture-backed startups, valuers may agree to part of their fee being settled in equity or convertible instruments. This aligns incentives but is subject to regulatory and ethical considerations.

Such flexibility allows businesses to manage cash flows better while ensuring compliance and investor readiness

Comparing Valuation Fees: Banks vs Private Firms

Companies often face a choice between engaging a bank-affiliated valuation unit or a private valuation firm, each with distinct pricing philosophies:

- Structured Caps (Banks): Public sector and institutional banks generally follow pre-defined fee caps or slab-based schedules, making costs more predictable. This can be advantageous for SMEs or borrowers who need valuations for lending or regulatory purposes.

- Market-Driven Rates (Private Firms): Independent valuation firms operate on competitive pricing, with fees reflecting the complexity of the assignment, sector expertise, and brand reputation. While potentially higher, these firms often provide faster turnaround, tailored advisory, and greater flexibility.

Pros for Banks: Transparent and capped fees, regulatory alignment, wide acceptance with lenders.

Cons for Banks: Limited flexibility, longer turnaround, less sector-specific expertise.Pros for Private Firms: Customised analysis, faster execution, broader scope of services (e.g., cross-border, ESOP, PPA).

Ultimately, the choice depends on whether the company prioritises cost certainty (banks) or specialised expertise and speed (private firms)

Cons for Private Firms: Fees can escalate for complex or urgent assignments; negotiations may be required.

Best Practices for Companies Budgeting Valuation Costs

Navigating valuation fees requires foresight and structured planning. Companies can optimise costs by adopting the following practices:

- Aligning with Regulatory Requirements: Before engaging a valuer, confirm whether the exercise is legally mandatory (e.g., under the Companies Act, FEMA, or Income Tax Act). This avoids over-scoping and ensures compliance without incurring unnecessary expenses.

- Clarifying Scope in Engagement Letters: Clearly define the purpose, methodology, and deliverables in the engagement letter. A well-drafted scope reduces scope creep, which is a frequent cause of fee escalation.

- Planning for Repeat or Annual Valuations: For startups and firms undergoing multiple funding rounds or recurring ESOP issuances, negotiating multi-year retainers or bundled packages often results in lower per-assignment costs.

By proactively managing scope and timelines, companies can balance affordability with compliance.

Conclusion: Understanding the ‘Fair Range’ in 2025

Valuation fees in India, while guided by regulatory frameworks, remain highly contextual. At one end, statutory minimums under Rule 8C start as low as ₹500. At the other, large corporate valuations—particularly those involving listed entities, M&A, or complex group structures—can stretch into ₹10 lakhs or more.

For most companies in 2025, the fair range sits between ₹50,000 and ₹2.5 lakhs, depending on size, complexity, and the choice between bank-affiliated or private firms. Transparency, regulatory alignment, and effective negotiation remain the three pillars for ensuring value-for-money in this critical exercise.

Frequently Asked Questions (FAQs)

As per Rule 8C of the Wealth Tax Rules (adopted under the Companies Act), the minimum statutory fee is ₹500. However, actual market practice is usually higher.

For early-stage startups, fees generally range from ₹25,000 to ₹1 lakh, depending on complexity, number of shareholders, and whether the purpose is fundraising, ESOP issuance, or compliance.

Yes. Public sector banks often use slab-based fee caps (e.g., ₹5,000–₹50,000, with a ceiling of ₹1.5 lakhs), while private firms follow market-driven pricing that may be higher but offers faster execution and more customised expertise.

No. In addition to the valuer’s professional fee, companies must factor in 18% GST, along with travel, site visits, or due diligence expenses, especially for large or multi-location assignments.

Yes. Many firms offer scope-based discounts for startups, multi-year retainers for recurring valuations, or even milestone-linked billing. In select cases, equity-linked fee models are also possible for VC-backed companies.