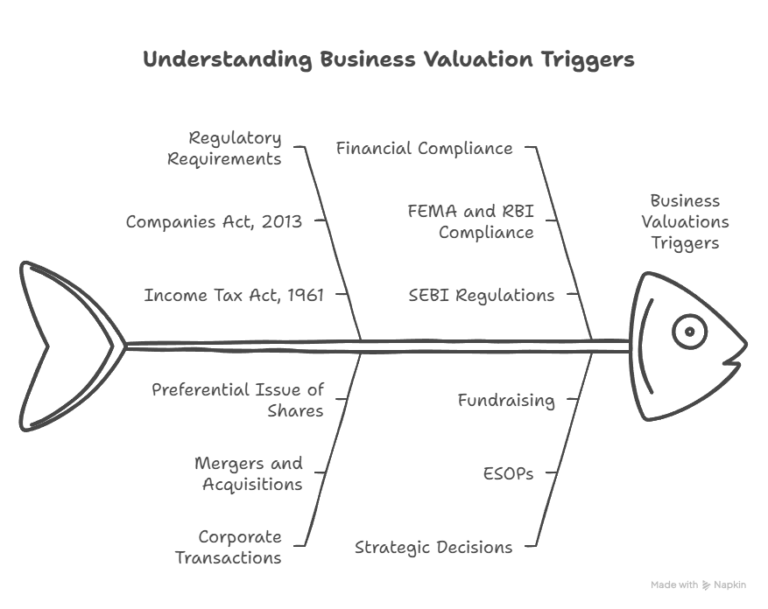

Business valuation is mandatory under various provisions of the Companies Act, 2013, such as during preferential allotment of shares, mergers and demergers, acquisition of minority shareholding, non-cash transactions, and liquidation. It is also required under the Income Tax Act, FEMA, and SEBI regulations in specific scenarios.