Table of Contents

Toggle1.Introduction

A Venture Capital (VC) valuation report is a structured, comprehensive document that estimates the economic value of a startup or early-stage company. Far from being just a number on paper, it serves as a strategic tool that informs crucial business decisions. In India’s dynamic startup ecosystem, a well-prepared VC valuation report provides clarity and confidence to founders, investors, and regulators alike.

For Indian startups, the importance of a VC valuation report cannot be overstated. First and foremost, it plays a pivotal role in fundraising, helping entrepreneurs communicate the fair value of their company to venture capitalists, angel investors, or private equity firms. It also ensures regulatory compliance, particularly under Indian laws such as the Companies Act 2013, SEBI regulations, and the Income Tax Act, thereby protecting the company from legal and tax-related risks. Beyond fundraising and compliance, these reports are crucial during mergers and acquisitions (M&A), providing a defensible valuation basis that supports negotiations. Internally, a valuation report offers startup leadership an objective assessment of business performance and growth potential, assisting in strategic planning, resource allocation, and performance benchmarking.

By laying out a structured, transparent approach to valuing a startup, a VC valuation report establishes a professional framework that fosters trust among investors and aligns expectations between all stakeholders.

2.Background Information of the Company

The background section of a VC valuation report provides a foundational understanding of the company, enabling readers to contextualize the valuation. It typically begins with a concise overview of the company’s history and founding team, highlighting key milestones such as inception, product launches, major client acquisitions, and strategic pivots. A clear description of the business model—whether it is SaaS, fintech, edtech, or another segment—helps investors understand how the company generates revenue, manages costs, and scales operations.

Next, the report outlines the company’s current ownership structure and capital composition, including equity distribution among founders, employees, and existing investors. This section also details any previous funding rounds, specifying the type of investment, valuation at the time, and investor participation.

Equally important is the disclosure of the appointing authority—the entity or individual who commissioned the report—and the intended users, which may include prospective investors, financial institutions, regulatory authorities, or internal management teams. Clearly defining the intended audience ensures that the valuation report maintains relevance, complies with statutory requirements, and effectively supports the specific decision-making context for which it was prepared.

3.Purpose of the Report & Regulatory Context

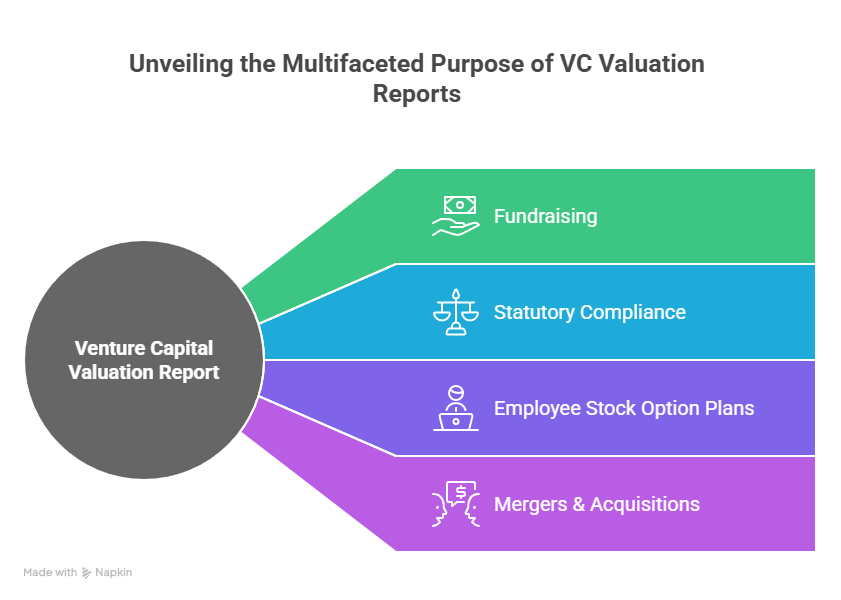

The purpose of a Venture Capital valuation report must be clearly articulated, as it guides both the methodology and the interpretation of results. Typically, such a report is prepared for multiple strategic objectives:

- Fundraising: To determine a fair pre-money or post-money valuation when seeking capital from venture capitalists, angel investors, or private equity firms.

- Statutory Compliance: To meet regulatory requirements for share allotments, capital increases, or other corporate actions.

- Employee Stock Option Plans (ESOPs): To establish the fair value of shares for granting options to employees, in line with tax and legal guidelines.

- Mergers & Acquisitions (M&A): To provide a defensible, objective basis for negotiations and transaction structuring.

In India, VC valuation reports must comply with specific regulatory frameworks to ensure legality and credibility. Key references include:

- FEMA (Foreign Exchange Management Act): Governs inbound foreign investments and valuation norms for pricing shares.

- Companies Act 2013: Mandates proper valuation for private placements, preferential allotments, and capital increases.

- Income Tax Act, Section 56(2)(viib): Prescribes taxation guidelines when shares are issued at a premium above the fair market value.

- SEBI Guidelines: Applicable when valuations are linked to listed entities, venture capital funds, or regulated investment activities.

Equally critical is the credentials of the valuer preparing the report. In India, this may include a SEBI-registered Merchant Banker, an ICAI-registered Chartered Accountant, or an IBBI-registered Valuer. Proper disclosure of credentials ensures that the report is legally recognized and instills confidence among investors and regulators.

4.Valuation Approaches & Methodologies

A VC valuation report derives its credibility from a clearly documented valuation methodology, selected based on the startup’s stage, sector, and financial profile. The most commonly applied approaches in India include:

1.Discounted Cash Flow (DCF) Method:

- Projects the startup’s future cash flows over a defined period (typically 3–5 years).

- Discounts these cash flows to present value using an appropriate cost of capital, reflecting business risk.

- Provides an intrinsic value of the company based on its projected operational performance.

2.Mergers, Acquisitions, and Corporate Restructuring

- Compares the startup with similar companies or recent transactions in the same industry.

- Uses financial multiples such as EV/Revenue, EV/EBITDA, or P/E ratios to benchmark value.

- Particularly useful when market data is available and comparable startups exist.

3.Net Asset Value (NAV) / Asset-Based Method:

- Values the company based on the fair market value of its assets minus liabilities.

- Typically applied when tangible assets are significant or for early-stage companies with limited revenue.

The report should also justify why certain methods are included or excluded. For instance, DCF may not be reliable for pre-revenue startups, while NAV might undervalue high-growth digital ventures.

Finally, the report must explain how key financial metrics are calculated, including revenue projections, EBITDA margins, and discount rates. Transparent documentation of assumptions, calculation methods, and adjustments ensures that investors and regulators can understand and trust the derived valuation.

5.Financial Analysis & Projections

A robust VC valuation report relies heavily on a thorough financial analysis to support the estimated value of the company. This begins with a detailed review of audited historical financial statements, including the income statement, balance sheet, and cash flow statements. These documents provide an objective record of past performance, highlighting revenue growth, profitability, cash generation, and capital utilization.

Building on historical performance, the report includes projected financial statements for a period of three to five years. These projections typically cover revenue, EBITDA, net profit, and cash flows. They reflect management’s strategic plans, expected market growth, and operational scalability, while also allowing investors to model potential returns.

Crucial to the credibility of these projections are the assumptions underpinning them, such as expected growth rates, profit margins, funding requirements, and capital expenditures. The report must clearly document these assumptions, explaining the rationale behind each figure, and indicate the level of confidence in the projections. Transparent presentation of assumptions ensures that investors, regulators, and stakeholders can assess both the opportunity and the associated risks.

6.Market & Competitive Analysis

Understanding the market environment is essential for determining a startup’s potential value. The market and competitive analysis section of a VC valuation report examines the industry landscape, emerging trends, and the total addressable market (TAM). It provides insights into market size, growth projections, and segmentation, offering investors a sense of scale and opportunity.

The report also benchmarks the startup against its peers, analyzing factors such as product differentiation, market share, customer acquisition strategy, and revenue performance. Both qualitative insights (like brand positioning and strategic partnerships) and quantitative metrics (like market penetration, growth rates, and competitor valuations) are included to offer a comprehensive view of the startup’s competitive positioning.

This analysis helps investors understand the startup’s relative strengths, weaknesses, and the market dynamics that may influence its future performance. By integrating both market and financial perspectives, the valuation report delivers a well-rounded assessment of the company’s growth potential and investment attractiveness.

7.Risk Assessment

A comprehensive VC valuation report does not stop at estimating value—it must also provide a candid evaluation of the risks associated with the business. These risks generally fall into three categories:

- Operational Risks: Challenges related to day-to-day business operations, including production, supply chain, technology, and talent retention.

- Regulatory Risks: Potential exposure to changing laws, tax regulations, or compliance requirements under Indian statutes such as the Companies Act 2013, FEMA, and SEBI regulations.

- Market Risks: External factors like competitive pressures, shifting customer preferences, macroeconomic conditions, and market volatility that could impact growth.

The report should also outline mitigation strategies, reflecting management’s approach to addressing these risks, such as contingency planning, insurance coverage, diversification, or regulatory compliance programs. Including management commentary ensures transparency and demonstrates that risks are acknowledged and actively managed.

For investors and regulators, this section is critical. It highlights potential challenges that may affect the startup’s future performance, allowing stakeholders to make informed decisions and evaluate whether the risk-adjusted valuation aligns with their expectations.

8.Key Assumptions & Limitations

Every VC valuation report is built on a framework of explicit assumptions, which provide the foundation for projections and methodologies. Common assumptions include:

- Market Growth: Expected expansion of the target market and the startup’s projected market share.

- Regulatory Stability: Anticipated consistency in legal and tax frameworks that affect business operations.

- Customer Concentration: Estimates regarding revenue dependency on key clients and potential diversification risks.

Alongside these assumptions, the report must include caveats and disclaimers. These may relate to the reliability of management projections, the accuracy of market data, or limitations in available financial information.

Crucially, these assumptions directly influence the valuation outcome. Transparent disclosure ensures that investors and regulators understand the basis of the estimated value, the sensitivity of projections to underlying assumptions, and the potential for variance in future performance.

9.Due Diligence & Procedures

A credible VC valuation report is underpinned by rigorous due diligence. This process ensures that the valuation is based on verified, reliable information rather than assumptions alone. Key steps typically include:

- Site Visits: Physical inspection of facilities, offices, or operational locations to validate assets and operations.

- Management Interviews: Discussions with founders, senior management, and key personnel to understand business strategy, risks, and future plans.

- Third-Party Data Verification: Validation of market data, competitor information, legal compliance, and financial statements through external sources.

The report should also clearly state the extent of reliance on company-provided information, specifying which data were internally sourced versus independently verified. Any limitations in due diligence, such as restricted access to certain documents or reliance on unverified projections, must be transparently disclosed. This level of clarity provides stakeholders with confidence in the integrity of the valuation while setting realistic expectations regarding its limitations.

10.Valuation Conclusion & Executive Summary

A credible VC valuation report is underpinned by rigorous due diligence. This process ensures that the valuation is based on verified, reliable information rather than assumptions alone. Key steps typically include:

- Site Visits: Physical inspection of facilities, offices, or operational locations to validate assets and operations.

- Management Interviews: Discussions with founders, senior management, and key personnel to understand business strategy, risks, and future plans.

- Third-Party Data Verification: Validation of market data, competitor information, legal compliance, and financial statements through external sources.

The report should also clearly state the extent of reliance on company-provided information, specifying which data were internally sourced versus independently verified. Any limitations in due diligence, such as restricted access to certain documents or reliance on unverified projections, must be transparently disclosed. This level of clarity provides stakeholders with confidence in the integrity of the valuation while setting realistic expectations regarding its limitations.

11.Regulatory Declarations & Compliance

A Venture Capital valuation report must clearly articulate regulatory declarations and compliance to ensure legal validity and build trust with investors and authorities. This section typically includes:

- Conflicts of Interest: Any potential or actual conflicts must be disclosed to maintain transparency and avoid biased valuation outcomes.

- Valuer’s Credentials: The qualifications and registration of the professional preparing the report, such as a SEBI-registered Merchant Banker, an IBBI-registered Valuer, or an ICAI-certified Chartered Accountant.

- Compliance with Standards: Confirmation that the report adheres to established ICAI Valuation Standards, IBBI guidelines, and SEBI regulations, ensuring that the methodology, reporting, and assumptions meet statutory requirements.

- Usage & Distribution Restrictions: Specific instructions on how the report may be used, shared, or relied upon, highlighting any limitations to prevent misuse or misinterpretation by third parties.

This section assures stakeholders that the valuation has been conducted in a professional, legally compliant manner, providing a defensible basis for investment decisions or regulatory filings.

12.Annexures & Supporting Documents

To enhance transparency and provide detailed context, a VC valuation report includes annexures and supporting documents. Typical inclusions are:

- Engagement Letter: Outlining the scope of the valuation, responsibilities, and terms of engagement between the valuer and the company.

- Detailed Calculations: Comprehensive numerical work, including DCF models, market multiple analyses, and NAV computations.

- Management Representations: Statements from the company’s management affirming the accuracy and completeness of the information provided.

- Regulatory Filings: Copies or references to relevant filings, approvals, or statutory documents used in the valuation process.

- Key Definitions & Methodology Appendices: Glossary of technical terms, explanations of valuation methods, and supporting assumptions for investor clarity.

Including these annexures ensures that the valuation report is transparent, well-documented, and easily auditable, providing all stakeholders—investors, regulators, and internal teams—with the confidence that the valuation process is both robust and credible.

Frequently Asked Questions (FAQs)

A VC valuation report provides an independent estimate of a startup’s value. It is primarily used for fundraising, regulatory compliance, employee stock option plans (ESOPs), mergers and acquisitions (M&A), and strategic decision-making.

In India, such reports must be prepared by qualified professionals such as SEBI-registered Merchant Bankers, IBBI-registered Valuers, or ICAI-certified Chartered Accountants, depending on the regulatory requirement.

The most commonly applied methods include: Discounted Cash Flow (DCF), Market Multiples / Comparable Company Analysis, and Net Asset Value (NAV). The choice depends on the startup’s stage, industry, and available data.

Due diligence ensures that the valuation is based on verified and reliable data. It involves site visits, management interviews, and third-party data verification, and it helps identify risks and validate assumptions.

Annexures typically include the engagement letter, detailed calculations, management representations, relevant regulatory filings, methodology appendices, and definitions of key terms. These documents enhance transparency and credibility of the report.